The 2026 Roth Revolution: Why Your Clients Need a 'Pivot' Strategy Now

- Jud Tolmen

- Feb 19

- 5 min read

Here's something most people don't realize: $48 trillion sits in retirement accounts across America right now. Nearly $19 trillion of that is locked up in IRAs: and the vast majority of it has never been taxed.

Not once.

That's not a loophole. That's a tax bill waiting to happen. And for your clients, 2026 is the year to take control of when, how much, and at what rate they're going to pay Uncle Sam.

If you're not talking Roth conversions with your clients right now, you're leaving serious money: and serious opportunities: on the table.

The Big Shift Nobody Saw Coming

For years, the conventional wisdom was simple: "Wait until retirement when you're in a lower tax bracket." The entire 401(k) system launched in 1981 on that premise.

But here's the problem: it didn't work out that way for most people.

Thanks to RMDs (Required Minimum Distributions), Social Security taxation, pension income, and the fact that many retirees have more money than they thought: plenty of folks are sitting in the same or higher tax brackets in retirement than they were during their working years.

Add in Medicare premium surcharges (IRMAA), potential estate taxes, and the reality that tax rates could shift at any time, and you've got a recipe for a very expensive retirement surprise.

That's where the Roth conversion pivot comes in: and why 2026 is a golden window.

The Strategy: Transfer, Convert, and Let It Grow Tax-Free

Here's the play, and it's simpler than most people think.

Let's say you've got a client: John, age 59½, just separated from his employer. He's sitting on $500,000 in his old 401(k), and it's all pre-tax money. Every dollar he pulls out in retirement will be taxed as ordinary income.

But here's what John doesn't know: He has options. Smart ones.

The $50,000 Roth Conversion Move

Instead of leaving that $500k to grow and compound into an even bigger tax problem down the road, we help John do this:

Step 1: Transfer $50,000 from his 401(k) to an IRA with one of our partner companies: Equitrust, American Equity, or another carrier we work with. This is a straightforward rollover. No tax event yet.

Step 2: Convert that $50,000 IRA into a Roth IRA. Now we've triggered a taxable event, but it's controlled and planned.

Step 3: John pays the tax bill now: in his case, he's in the 22% tax bracket, so that's $11,000 in federal taxes due.

Ouch, right? But here's the kicker: That $50,000 is now growing tax-free. Forever.

No RMDs. No tax bombs at age 73. No surprise IRMAA surcharges. And when John pulls that money out in retirement: or leaves it to his kids: it's 100% tax-free.

The Math That Changes Everything

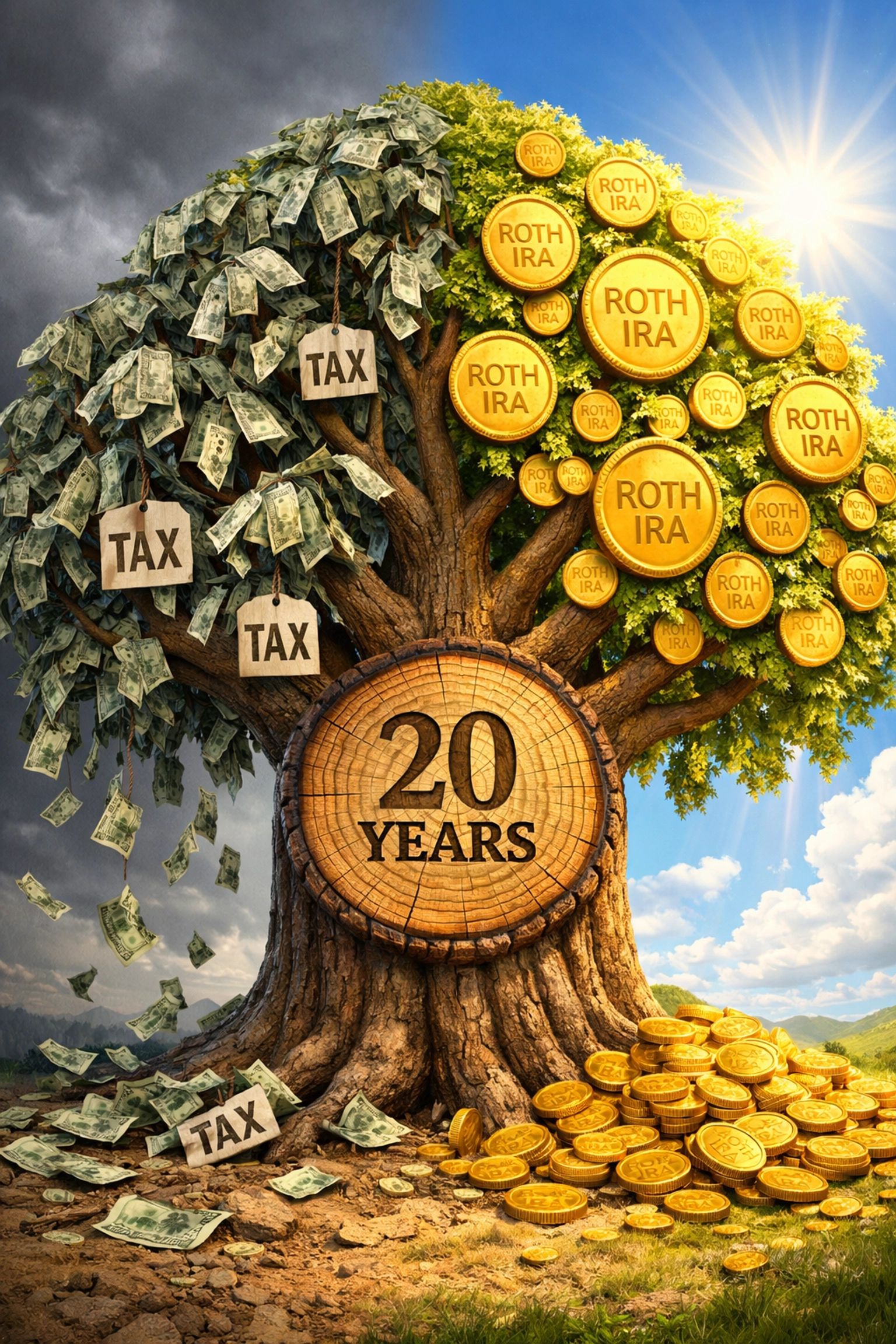

Let's zoom out for a second. If John leaves that $500k in his 401(k) and lets it grow at a modest 6% annually, in 20 years he's looking at over $1.6 million. Awesome, right?

Except every single dollar of that $1.6 million is taxable. If tax rates go up (and let's be honest, they probably will), or if his RMDs push him into a higher bracket, he could easily be paying 30%+ on those distributions.

That's a $480,000+ tax bill on the back end.

Now compare that to the $11,000 he pays today on the $50k Roth conversion. That converted amount grows to $160,000 in 20 years: completely tax-free. And if John does a series of strategic conversions over the next 5-10 years? He can systematically move large chunks of that 401(k) into the Roth bucket, paying taxes at today's known rates and locking in decades of tax-free growth.

The "Forever Taxed" vs. "Never Taxed" Bucket

Think of it this way:

Forever Taxed: Traditional 401(k)s, IRAs, pensions. Every dollar you pull out gets taxed. Forever.

Never Taxed: Roth IRAs, Roth conversions done right. You pay the tax once, and then it's done. Never taxed again.

Which bucket would your clients rather have in retirement?

Why 2026 Is the Year to Act

Here's what makes 2026 such a critical year for Roth conversions:

1. RMD Rules Have Shifted RMDs now start at age 73 (and will move to 75 for those born in 1960 or later). That gives clients a longer runway to do strategic conversions before they're forced to start taking taxable distributions.

2. Tax Rates Are Locked (For Now) Thanks to recent legislation, the Tax Cuts and Jobs Act rates are extended. The 22% bracket? That's a known quantity right now. Lock it in while you can, because tax policy is always one election away from changing.

3. Bonus Deductions for Older Clients Clients age 65+ get bonus standard deductions, which means they can potentially convert larger amounts at lower effective tax rates. It's a narrow window, and it won't last forever.

4. Medicare and IRMAA Planning Doing conversions before clients hit Medicare age can help them avoid IRMAA surcharges later. One well-timed conversion beats five years of elevated Medicare premiums.

How to Present This to Your Clients

This isn't a hard sell. It's a conversation about control.

"Would you rather pay taxes on $50,000 today, or $500,000 later? Because one way or another, the IRS is getting paid."

Walk them through the numbers. Show them the difference between paying 22% now versus 30%+ later. Explain that this isn't about avoiding taxes: it's about choosing when and how much they pay.

And here's the best part: The paperwork is simple. You help them transfer funds from their current 401(k) or IRA to one of our partner companies, file the Roth conversion, and boom: they've just bought themselves decades of tax-free growth.

Your Role in This

As agents, this is where you shine. Your clients don't know these strategies exist. They don't know that "Forever Taxed" money can become "Never Taxed" money with a little planning and the right guidance.

That's where Tolmen Financial comes in. We help you understand how to work both ends: minimizing the tax hit today while maximizing the tax-free growth tomorrow. No matter your client's age, income, or situation, there's a pivot strategy that fits.

Whether your client has $50k or $5 million in qualified accounts, the principle is the same: Control the tax bill. Maximize the tax-free growth. Build a better retirement.

Let's Make This Happen

If you've got clients sitting on pre-tax retirement accounts: and let's be honest, you do: 2026 is the year to have the Roth conversion conversation.

We've got the tools, the carriers, and the strategy to make this seamless. Equitrust, American Equity, and our full roster of partners are ready to help you execute these conversions with confidence.

Want to dive deeper? Check out our resources at TolmenFinancial.com/million or reach out directly.

Judson Tolmen President, Tolmen Financial 📧 Jud@TolmenFinancial.com 📞 (219) 608-5498

Let's swing that pendulum in the right direction: and help your clients build the tax-free retirement they deserve.

Comments